Backtesting that lives in Excel.

Test rules-based stock strategies without learning Python or paying SaaS

rent.

Test rules-based stock strategies without learning Python or paying SaaS

rent.

StrategyXL lives where you already work. No new app to learn, no exported CSVs, no platform lock-in. Click a button, fill a template, get a result.

MA Crossover, Price vs MA, MACD, RSI, Stochastic, Channel breakout, and Bollinger Bands. Pick a strategy, set the parameters, run.

Combine stop-losses, take-profits, signal-based exits, and time-based exits — without writing a single line of code.

Run the same strategy across hundreds of tickers in a single click. Compare results side-by-side in one workbook.

Lock your favorite parameter sets per signal type. Reload them on demand. No more re-typing dates and tickers.

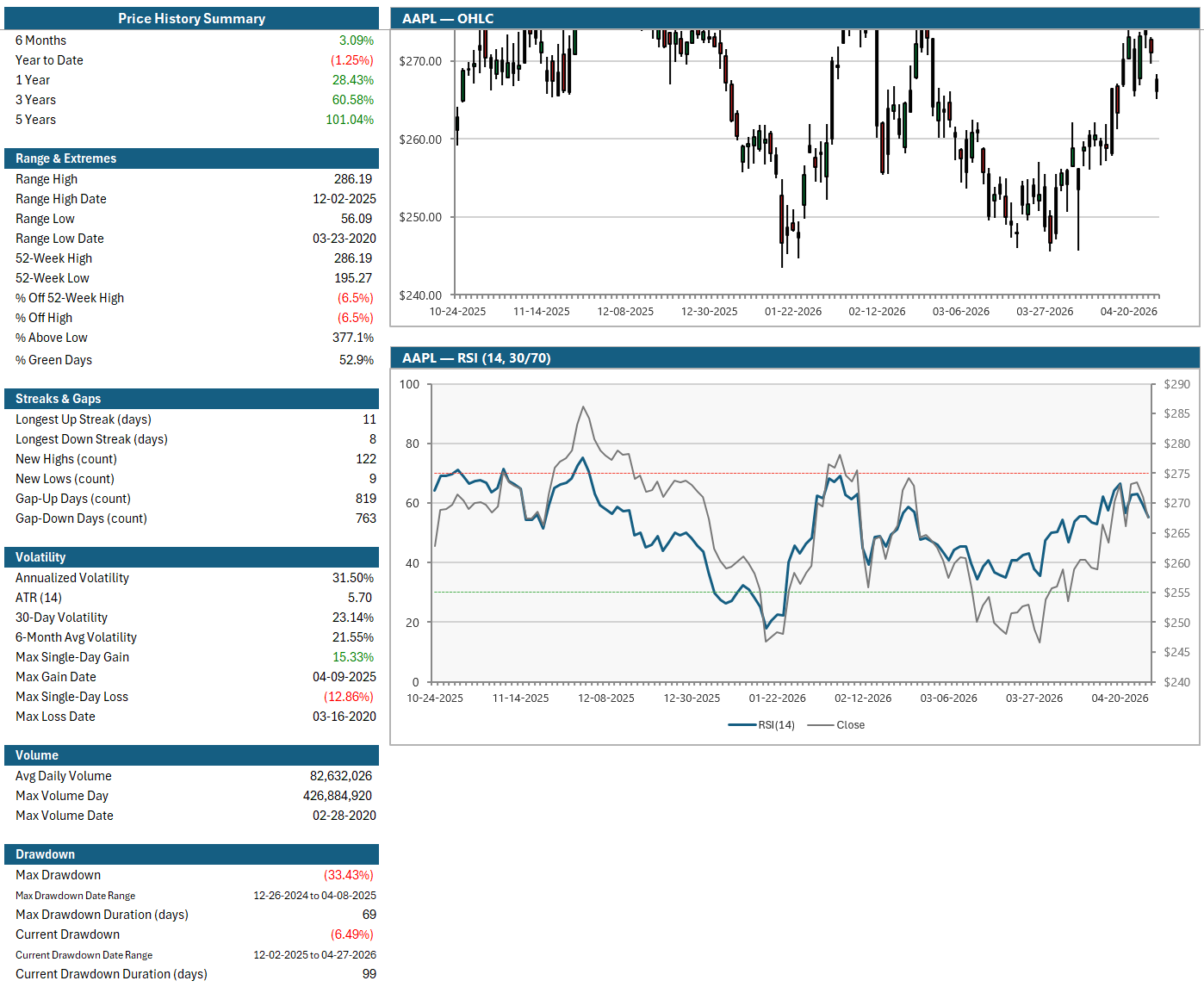

Price History fetches OHLCV data and renders RSI, MACD, Bollinger Bands, Stochastic, and moving averages as Excel charts automatically.

Every backtest is auto-saved. Filter, sort, and re-render past runs without re-fetching data — right inside Excel.

The roadmap

StrategyXL's core platform is paid-once, not subscription, so I don't need to manufacture features to justify monthly fees — I just build what users actually ask for. The roadmap is open: see what's coming, send your own ideas, and help shape what I ship next.

Install once. Backtest forever. One price for the core platform, all v1 updates included — no subscription required, no usage limits, no surprises.